Laws, Regulations, and Annotations

Lawguide Search

Business Taxes Law Guide—Revision 2026

Sales And Use Tax Regulations

Title 18. Public Revenues

Division 2. California Department of Tax and Fee Administration — Business Taxes

Chapter 4. Sales and Use Tax

Article 3. Manufacturers, Producers, Processors

Regulation 1533

Regulation 1533. Liquefied Petroleum Gas.

Reference: Section 6353, Revenue and Taxation Code.

(a) General. Commencing on and after September 1, 2001, Section 6353(b) of the Revenue and Taxation Code exempts from sales and use tax the sale of, and the storage, use, or other consumption in this state, of qualified LPG used by a qualified person in an agricultural activity, or used in a qualified residence for a household activity. The terms "qualified LPG," "qualified person," "agricultural activity," "qualified residence," and "household activity" are defined below.

(b) Definitions. For purposes of this regulation:

(1) "Agricultural activity" means the producing and harvesting of agricultural products as defined in subdivision (b)(4), by a qualified person as defined in subdivision (b)(5).

(2) "Household activity" means those activities normally undertaken in a qualified residence as defined in subdivision (b)(7), such as cooking, heating and lighting.

(3) "Person that assists a qualified person" means a person employed by a qualified person, or engaged on a contract or fee basis to perform activities described in Major Group 07 of the Standard Industrial Classification Manual published by the United States Office of Management and Budget, 1987 edition (hereafter SIC Manual) which include soil preparation services, crop services, veterinary services, animal services, landscape and horticultural services, and farm labor and management services, that uses qualified LPG in assisting a person engaged in a line of business described in subdivision (b)(5). A person that assists a qualified person may perform a construction contract only if the person performing the contract is engaged in farm management services as described in Code 0762 of the SIC Manual and the construction is integral to the producing and harvesting of an agricultural product as defined in (b)(4). A person that assists a qualified person must provide physical aid or assistance in the actual producing and harvesting of agricultural products owned by the qualified person and not merely provide aid in administrative, managerial, or marketing activities. A person that assists a qualified person does not include persons performing services such as an attorney, accountant, consultant, or other similar activity. Except as otherwise provided above, a person that assists a qualified person also does not include persons who perform construction contracts or who perform repairs to farm equipment and machinery, or a person who assists such persons.

(4) "Producing and harvesting agricultural products" means those activities described in Major Groups 01, 02 and 07 of the SIC Manual. Major Group 01 includes establishments engaged in the production of crops, plants, vines, and trees (excluding forestry operations). This major group also includes establishments engaged in the operation of sod farms; in the production of mushrooms, bulbs, flower seeds, and vegetable seeds; and in the growing of hydroponic crops. Major Group 02 includes establishments engaged in the keeping, grazing, or feeding of livestock for the sale of livestock or livestock products (including serums), for livestock increase, or for value increase. Livestock, as specified in Major Group 02, includes cattle, hogs, sheep, goats, and poultry of all kinds; also included are animal specialties, such as horses, rabbits, bees, pets, fish in captivity, and fur-bearing animals in captivity. Major Group 07 includes establishments engaged in performing soil preparation services, crop services, veterinary services, animal services, landscape and horticultural services, and farm labor and management services. Producing and harvesting agricultural products involves the cultivation of land or the growing, raising, or gathering of the commodities described in Codes 0111 to 0291 of the SIC Manual and integral activities thereto described in Codes 0711 to 0783 of the SIC Manual. Such activities include, but are not limited to, flame weeding, pest control, nut hulling and shelling, crop drying, cotton ginning, poultry and pig brooding, livestock breeding, water heating, crop heating, and fruit ripening. Producing and harvesting agricultural products also includes the washing of agricultural products, the inspection and grading of agricultural products or livestock, or the packaging of agricultural products for shipment. Except as otherwise provided under Major Groups 01, 02 or 07 of the SIC Manual, producing and harvesting activities do not include post harvesting activities nor those activities described or otherwise designated in Major Group 20—Food and Kindred Products of the SIC Manual. Nevertheless, the specific activities of sun drying or artificially dehydrating fruits and vegetables as described in Code 2034 of the SIC Manual qualify as producing and harvesting activities where those activities are performed by a qualified person as defined in (b)(5) or a person who assists a qualified person as defined in (b)(3).

Example A: Grower A farms raisins and uses qualified LPG to dry Grower A's raisins. Grower A is a qualified person (Code 0172 of the SIC Manual) and uses qualified LPG in the producing and harvesting of an agricultural commodity. The sale of qualified LPG to Grower A for use in this activity is exempt from tax.

Example B: Grower B farms plums and contracts with ABC, Inc. to dry the plums owned by Grower B in preparation for sale. ABC, Inc. uses qualified LPG to dry the plums. ABC, Inc. is a person assisting a qualified person (Code 0723 of the SIC Manual) such that the sale of qualified LPG to ABC for use in this activity is exempt from tax.

Example C: Grower C farms corn. Grower C sells the "wet" corn to a food processor based on the net dry weight of the product. The food processor uses qualified LPG to dry the corn. The food processor's use of qualified LPG to dry the commodity is not a qualified use since the food processor owns the commodity and thereby only performs a non-qualified, post harvesting activity. The sale of qualified LPG to the food processor for use in this activity is not exempt from tax.

(5) "Qualified person" means a person who purchases qualified LPG that is engaged in a line of business described in Codes 0111 to 0291 of the SIC Manual or performs activities described in Codes 0711 to 0783 in addition to being engaged in a line of business described in Codes 0111 to 0291, which includes cash grains, field crops, vegetables and melons, fruits and tree nuts, horticultural specialties, livestock, dairy, poultry and eggs, and animal specialties and who sells such commodities to others. A qualified person also includes any person conducting activities, as defined in subdivision (b)(3), that uses qualified LPG to assist a person engaged in a line of business described herein in producing and harvesting agricultural products owned by the qualified person. A qualified person is not required to be engaged 50 percent or more of the time in a line of business described in Codes 0111 to 0291. A qualified person does not include a person operating a garden plot, orchard, or farm for the purpose of growing produce or animals for that person's own use.

(6) "Qualified LPG" means liquefied petroleum gas delivered into a tank with a storage capacity that is equal to or greater than 30 gallons. Liquefied petroleum gas is a mixture of light hydrocarbons which are gaseous at atmospheric temperature and pressure. Liquefied petroleum gas occurs naturally in crude oil and natural gas production fields and is also produced in the oil refining process. Its main components are Propane (C3H8) at a boiling point of -42.07° and Butane (C4H10) at a boiling point of 0°. Delivery into tanks smaller than 30 gallons do not qualify for the exemption even if the total delivery exceeds 30 gallons.

(7) "Qualified residence" means a primary residence not serviced by gas mains and pipes, to which qualified LPG is delivered by a seller. A primary residence means a person's domicile where that person spends the greatest portion of his or her time during a calendar year. A person may change his or her primary residence only when that person moves from and otherwise abandons his or her previous residence and has no intent to return to that previous residence. In no event shall a primary residence include multiple residences maintained simultaneously such as a second, or vacation home.

Solely for purposes of this regulation, a qualified residence also includes a residence where qualified LPG is purchased by a qualified person for use in a household activity at the primary residence of:

(A) A person that assists a qualified person; or

(B) An employee of a qualified person where such person that assists a qualified person or employee of a qualified person performs an agricultural service described in Codes 0711 to 0783 of the SIC Manual for the qualified person. In addition, solely for purposes of this regulation, a qualified residence includes a residence where qualified LPG is purchased by a landlord or management company on behalf of a renter or tenant for use in a household activity at the primary residence of the renter or tenant.

(c) Exemption Certificates.

(1) In General. A person who purchases qualified LPG for use in an agricultural or household activity from an in-state retailer, or an out-of-state retailer obligated to collect use tax, must provide the retailer with an exemption certificate in order for the retailer to claim the exemption. If the retailer takes an exemption certificate timely and in good faith, as defined in subdivision (c)(5), from a purchaser, the exemption certificate relieves the retailer from the liability for the sales tax subject to exemption under this regulation or the duty of collecting the use tax subject to exemption under this regulation. An exemption certificate will be considered timely if it is taken any time before the retailer bills the purchaser for the qualified LPG, any time within the retailer's normal billing or payment cycle, any time at or prior to delivery of the qualified LPG to the purchaser, or no later than 15 days after the date of purchase. An exemption certificate which is not taken timely will not relieve the retailer of the tax liability; however the retailer may present satisfactory evidence to the Board that the retailer sold the qualified LPG to a purchaser for use in an agricultural or household activity. An exemption from the sales and use tax under this part shall not be allowed unless the retailer claims the exemption on its sales and use tax return for the reporting period during which the transaction subject to the exemption occurred. Where the retailer fails to claim the exemption as set forth above, the retailer may file a claim for refund as set forth in subdivision (e).

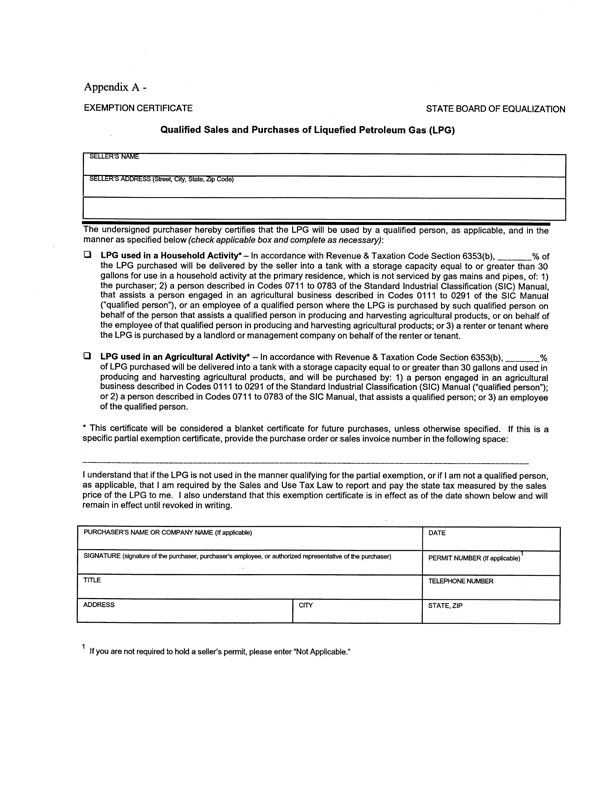

The exemption certificate form set forth in Appendix A may be used to claim the exemption.

(2) Blanket Exemption Certificates. In lieu of requiring an exemption certificate for each transaction, a person who purchases qualified LPG for use in an agricultural or household activity may issue a blanket exemption certificate. The exemption certificate form set forth in Appendix A may be used as a blanket exemption certificate. Appendix A may also be used as a specific exemption certificate if the purchaser provides the purchase order or sales invoice number and a precise description of the property being purchased. A person who purchases qualified LPG for use in an agricultural or household activity must include in the exemption certificate how much or what percentage of the qualified LPG will be used in the agricultural or household activity. If purchasing liquefied petroleum gas not qualifying for the exemption, the purchaser must clearly state in documents such as a written purchase order, sales agreement, lease, or contract that the sale or purchase is not subject to the blanket exemption certificate.

(3) Form of Exemption Certificate. Any document, such as a letter or purchase order, timely provided by the purchaser to the seller will be regarded as an exemption certificate with respect to the sale or purchase of the liquefied petroleum gas if it contains all of the following essential elements:

(A) The signature of the purchaser, purchaser's employee, or authorized representative of the purchaser.

(B) The name, address and telephone number of the purchaser.

(C) The number of the seller's permit held by the purchaser. Except as otherwise provided in subdivision (b)(7), if the purchaser is not required to hold a permit because the purchaser sells only property of a kind the retail sale of which is not taxable, e.g., food products for human consumption, or because the purchaser makes no sales in this state, the purchaser must include on the certificate a sufficient explanation as to the reason the purchaser is not required to hold a California seller's permit in lieu of a seller's permit number.

(D) A statement that:

1. Of the liquefied petroleum gas purchased, how much or what percentage will be delivered by the seller into a tank with a storage capacity equal to or greater than 30 gallons for use in a household activity at the primary residence, which is not serviced by gas mains and pipes, of:

a. The purchaser;

b. A person described in Codes 0711 to 0783 of the Standard Industrial Classification (SIC) Manual published by the United States Office of Management and Budget, 1987 edition, that assists a person engaged in an agricultural business described in Codes 0111 to 0291 of the SIC Manual ("qualified person") or an employee of a qualified person where the LPG is purchased by such qualified person on behalf of the person that assists that qualified person in producing and harvesting agricultural products or on behalf of the employee that assists a qualified person in producing and harvesting agricultural products; or

c. A renter or tenant where the LPG is purchased by a landlord or management company on behalf of the renter or tenant.

2. Of the liquefied petroleum gas purchased, how much or what percentage will be delivered into a tank with a storage capacity equal to or greater than 30 gallons for use in producing and harvesting agricultural products, and will be purchased by:

a. A person engaged in an agricultural business described in Codes 0111 to 0291 of the Standard Industrial Classification (SIC) Manual published by the United States Office of Management and Budget, 1987 edition, ("qualified person");

b. A person described in Codes 0711 to 0783 of the SIC Manual, that assists a qualified person; or

c. An employee of a qualified person.

(E) Date of execution of document.

(4) Retention and Availability of Exemption Certificates.

A retailer must retain each exemption certificate received from a qualified person for a period of not less than four years from the date on which the retailer claims an exemption based on the exemption certificate.

While the Board will not normally require the filing of the exemption certificate with a sales and use tax return, when necessary for the efficient administration of the Sales and Use Tax Law, the Board may on 30 days' written notice, require a retailer to commence filing with its sales and use tax returns copies of all exemption certificates. The Board may also require, within 45 days of the Board's request, retailers provide the Board access to any and all exemption certificates, or copies thereof, accepted for the purposes of supporting the exemption.

(5) Good Faith. A seller will be presumed to have taken an exemption certificate in good faith in the absence of evidence to the contrary. A seller, without knowledge to the contrary, may accept an exemption certificate in good faith where the purchaser states that the qualified LPG will be used in a qualified residence for a household activity or in which a qualified person states that the qualified LPG will be used for an agricultural activity. However, an exemption certificate cannot be accepted in good faith where the seller has knowledge that the LPG is not subject to an exemption, will not be otherwise used in an exempt manner, or where a person is not a qualified person when purchasing qualified LPG for an agricultural activity.

(d) Exemption Certificate for Use Tax. The exemption certificate must be completed by a purchaser to claim an exemption from use tax on purchases of qualified LPG for use in an agricultural or household activity from an out-of-state retailer not obligated to collect the use tax. An exemption from the use tax shall not be allowed unless the purchaser or retailer claims the exemption on its individual use tax return, sales and use tax return, or consumer use tax return for the reporting period during which the transaction subject to the exemption occurred. Where the purchaser or retailer fails to claim the exemption as set forth above, the purchaser or retailer may file a claim for refund as set forth in subdivision (e).

The purchaser who files an individual use tax return must attach a completed exemption certificate to the return. The purchaser who is registered with the Board as a retailer or consumer and files a sales and use tax return or consumer use tax return must, within 45 days of the Board's request, provide the Board access to any and all documents that support the claimed exemption.

The exemption certificate form set forth in Appendix A may be used to claim the exemption.

(e) Refund of Tax.

(1) For the period commencing on September 1, 2001, and ending on April 30, 2002, a purchaser may claim the exemption on qualified purchases from an in-state retailer or an out-of-state retailer obligated to collect the use tax by furnishing the retailer with an exemption certificate on or before July 31, 2002. The retailer must refund the tax or tax reimbursement directly to a qualified purchaser of qualified LPG or, at the purchaser's sole option, the purchaser may be credited with such amount.

(2) A retailer who paid sales tax on a qualified sale or a person who paid use tax on a qualified purchase and who failed to claim the exemption as provided by this regulation may file a claim for refund equal to the amount of the exemption that he or she could have claimed pursuant to this regulation. The procedure for filing a claim shall be the same as for other claims for refund filed pursuant to Revenue and Taxation Code section 6901. For transactions subject to use tax, a purchaser filing a claim for refund of the exemption has the burden of establishing that he or she was entitled to claim the exemption with respect to the amount of refund claimed under this part. For transactions subject to sales tax, a person filing a claim for refund of the exemption has the burden of establishing that the purchaser of qualified LPG for use in an agricultural or household activity otherwise met all the requirements of a qualified sale at the time of the purchase subject to the refund claimed under this part.

(f) Improper Use of Exemption.

(1) Property Used or Delivered in a Manner Not Qualifying for the Exemption. Tax applies to any sale of, and the storage, use, or other consumption in this state of liquefied petroleum gas that is used or delivered in a manner not qualifying for the exemption under this regulation.

(2) Purchases by Non-qualified Persons. Tax applies to any sale of, and the storage, use, or other consumption in this state of qualified LPG for use in an agricultural activity if the purchaser is not a qualified person.

(g) Purchaser's Liability for the Payment of Sales Tax.

(1) If a purchaser timely submits a copy of an exemption certificate to the retailer or exemption certificate for use tax to the Board, and then uses or takes delivery of the liquefied petroleum gas in a manner not qualifying for the exemption, the purchaser shall be liable for payment of the sales tax, with applicable interest, to the same extent as if the purchaser were a retailer making a retail sale of the liquefied petroleum gas at the time the liquefied petroleum gas was so removed, converted, or used.

(2) A purchaser providing an exemption certificate accepted in good faith by the retailer or an exemption certificate for use tax to the Board for liquefied petroleum gas that does not qualify for the exemption is liable for payment of the sales tax, with applicable interest, to the same extent as if the purchaser were a retailer making a retail sale of the liquefied petroleum gas at the time the liquefied petroleum gas was purchased.

(h) Records. Adequate and complete records must be maintained by the purchaser as evidence that the qualified LPG purchased was used in an agricultural or household activity.

(i) Effective Date. This regulation is effective as of September 1, 2001.

History—Adopted March 27, 2002, operative September 1, 2001.

Appendix A - Exemption Certificate State Board of Equalization Qualified Sales and Purchases of Liquefied Petroleum Gas (LPG)