Laws, Regulations and Annotations

Search

Business Taxes Law Guide—Revision 2024

Sales And Use Tax Regulations

Title 18. Public Revenues

Division 2. California Department of Tax and Fee Administration — Business Taxes (State Board of Equalization — Business Taxes — See Chapters 6 and 9.9)

Chapter 4. Sales and Use Tax

Article 3. Manufacturers, Producers, Processors

Regulation 1535

Regulation 1535. Racehorse Breeding Stock.

Reference: Section 6358.5, Revenue and Taxation Code.

(a) General. Commencing on and after September 1, 2001, section 6358.5 of the Revenue and Taxation Code partially exempts from sales and use tax the sale of, and the storage, use, or other consumption in this state, of racehorse breeding stock purchased for use by a qualified person. The terms "racehorse breeding stock" and "qualified person" are defined below.

For the period commencing on September 1, 2001 and ending December 31, 2001, the partial exemption applies to the taxes imposed by sections 6051 and 6201 of the Revenue and Taxation Code (4.75%), but does not apply to the taxes imposed pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

For the period commencing on January 1, 2002, and ending on June 30, 2004, the partial exemption applies to the taxes imposed by sections 6051, 6051.3, 6201, and 6201.3 of the Revenue and Taxation Code (5%), but does not apply to the taxes imposed pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

For the period commencing on July 1, 2004, and ending on March 31, 2009, the partial exemption applies to the taxes imposed by Sections 6051, 6051.3, 6051.5, 6201, 6201.3, and 6201.5 of the Revenue and Taxation Code (5.25%), but does not apply to the taxes imposed or administered pursuant to Sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or Section 35 of article XIII of the California Constitution.

For the period commencing on April 1, 2009, and ending on June 30, 2011, the partial exemption applies to the taxes imposed by sections 6051, 6051.3, 6051.5, 6051.7, 6201, 6201.3, 6201.5, and 6201.7 of the Revenue and Taxation Code (6.25%), but does not apply to the taxes imposed or administered pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

For the period commencing on July 1, 2011, and ending on December 31, 2012, the partial exemption applies to the taxes imposed by sections 6051, 6051.3, 6051.5, 6201, 6201.3, and 6201.5 of the Revenue and Taxation Code (5.25%), but does not apply to the taxes imposed or administered pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

For the period commencing on January 1, 2013, and ending on December 31, 2015, the partial exemption applies to the taxes imposed by section 36 of article XIII of the California Constitution and sections 6051, 6051.3, 6051.5, 6201, 6201.3, and 6201.5 of the Revenue and Taxation Code (5.50%), but does not apply to the taxes imposed or administered pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

For the period commencing on January 1, 2016, and ending on December 31, 2016, the partial exemption applies to the taxes imposed by section 36 of article XIII of the California Constitution and sections 6051, 6051.3, 6201, and 6201.3 of the Revenue and Taxation Code (5.25%), but does not apply to the taxes imposed or administered pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

For the period commencing on January 1, 2017, the partial exemption applies to the taxes imposed by sections 6051, 6051.3, 6201, and 6201.3 of the Revenue and Taxation Code (5%), but does not apply to the taxes imposed or administered pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

(b) Definitions. For purposes of this regulation:

(1) "Qualified person" means a person who purchases racehorse breeding stock solely with the intent and purpose of breeding.

(2) "Qualified property" means racehorse breeding stock, as defined in subdivision (b)(3).

(3) "Racehorse breeding stock" means a live horse that meets all of the following criteria:

(A) Is or will be eligible to participate in a horseracing contest in California wherein pari-mutuel wagering is permitted under rules and regulations prescribed by the California Horse Racing Board.

(B) Is capable of producing foals which will be eligible to participate in a horseracing contest in California wherein pari-mutuel wagering is permitted under rules and regulations prescribed by the California Horse Racing Board.

(C) Is or was registered with an agency recognized by the California Horse Racing Board and such registering agency does not register the horse as ineligible for breeding stock. Agencies currently recognized are The Jockey Club, The American Quarter Horse Association, The United States Trotting Association, The Appaloosa Horse Club, The Arabian Horse Registry of America, and the American Paint Horse Association.

Racehorse breeding stock does not include any horse over four years old, or five years old in the case of an Arabian horse, that has neither participated in or trained for a horserace contest on which pari-mutuel wagering is permitted, nor been used for breeding purposes in order to produce racehorses.

(4) "Solely" means 100 percent or "only."

(c) Partial Exemption Certificates.

(1) In General. Qualified persons who purchase or lease qualified property from an in-state retailer, or an out-of-state retailer obligated to collect use tax, must provide the retailer with a partial exemption certificate in order for the retailer to claim the partial exemption. If the retailer takes a partial exemption certificate timely and in good faith, as defined in subdivision (c)(5), from a qualified person, the partial exemption certificate relieves the retailer from the liability for the sales tax subject to exemption under this regulation or the duty of collecting the use tax subject to exemption under this regulation. A partial exemption certificate will be considered timely if it is taken any time before the retailer bills the purchaser for the qualified property, any time within the retailer's normal billing or payment cycle, any time at or prior to delivery of the qualified property to the purchaser, or no later than 15 days after the date of purchase. A partial exemption certificate which is not taken timely will not relieve the retailer of the liability for tax excluded by the partial exemption; however the retailer may present satisfactory evidence to the Board that the retailer sold the specific property to a qualified person and the property was used in a qualifying manner. A partial exemption from the sales and use tax under this part shall not be allowed unless the retailer claims the partial exemption on its sales and use tax return for the reporting period during which the transaction subject to the partial exemption occurred. Where the retailer fails to claim the partial exemption as set forth above, the retailer may file a claim for refund as set forth in subdivision (e).

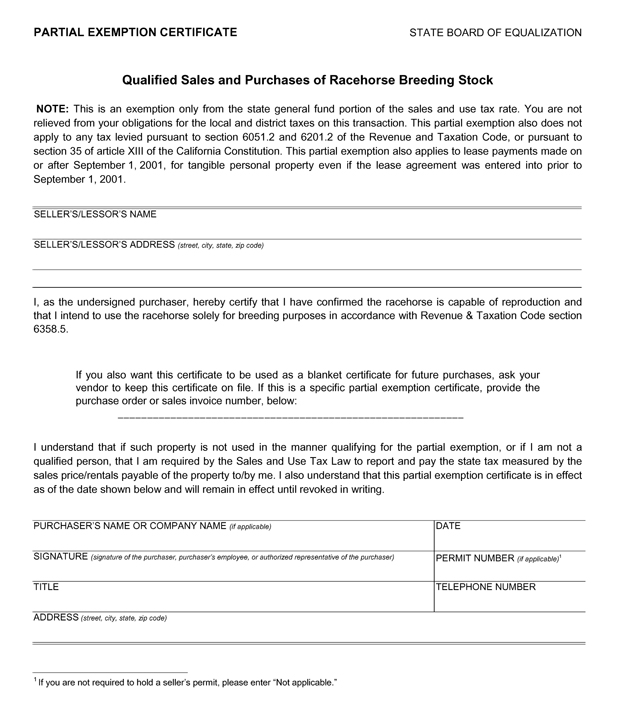

The partial exemption certificate form set forth in Appendix A may be used to claim the partial exemption.

(2) Blanket Partial Exemption Certificates. In lieu of requiring a partial exemption certificate for each transaction, a qualified person may issue a blanket partial exemption certificate. The partial exemption certificate form set forth in Appendix A may be used as a blanket partial exemption certificate. Appendix A may also be used as a specific partial exemption certificate if the purchaser provides the purchase order or sales invoice number of the property being purchased. Qualified persons must include in the partial exemption certificate a description of the qualified property. If purchasing tangible personal property not qualifying for the partial exemption, the qualified person must clearly state in documents such as a written purchase order, sales agreement, lease, or contract that the sale or purchase is not subject to the blanket partial exemption certificate.

(3) Form of Partial Exemption Certificate. Any document, such as a letter or purchase order, timely provided by the purchaser to the seller will be regarded as a partial exemption certificate with respect to the sale or purchase of the property described in the document if it contains all of the following essential elements:

(A) The signature of the purchaser, purchaser's employee, or authorized representative of the purchaser.

(B) The name, address and telephone number of the purchaser.

(C) The number of the seller's permit held by the purchaser. If the purchaser is not required to hold a permit because the purchaser sells only property of a kind the retail sale of which is not taxable, e.g., food products for human consumption, or because the purchaser makes no sales in this state, the purchaser must include on the certificate a sufficient explanation as to the reason the purchaser is not required to hold a California seller's permit in lieu of a seller's permit number.

(D) A statement that the property purchased is capable of reproduction.

(E) A statement that the purchaser will use the property solely for the purpose of breeding.

(F) A description of the property purchased.

(G) Date of execution of the document.

(4) Retention and Availability of Partial Exemption Certificates. A retailer must retain each partial exemption certificate received from a qualified person for a period of not less than four years from the date on which the retailer claims a partial exemption based on the partial exemption certificate.

While the Board will not normally require the filing of the partial exemption certificate with a sales and use tax return, when necessary for the efficient administration of the Sales and Use Tax Law, the Board may on 30 days written notice, require a retailer to commence filing with its sales and use tax returns copies of all partial exemption certificates. The Board may also require that, within 45 days of the Board's request, retailers provide the Board access to any and all partial exemption certificates, or copies thereof, accepted for the purposes of supporting the partial exemption.

(5) Good Faith. A seller will be presumed to have taken a partial exemption certificate in good faith in the absence of evidence to the contrary. A seller, without knowledge to the contrary, may accept a partial exemption certificate in good faith where a qualified person states that he or she is purchasing the qualified property solely with the intent and purpose of breeding. If the qualified person is buying a horse of a kind not normally used to breed racehorses, the seller should require a statement as to how the specific property purchased will be used. However, a partial exemption certificate cannot be accepted in good faith where the seller has knowledge that the property is not subject to the partial exemption, or will not be otherwise used in a partially exempt manner.

(d) Partial Exemption Certificate for Use Tax. The partial exemption certificate must be completed by a qualified person to claim a partial exemption from use tax on purchases of qualified property from an out-of-state retailer not obligated to collect the use tax. A partial exemption from the use tax shall not be allowed unless the purchaser or retailer claims the partial exemption on its individual use tax return, sales and use tax return, or consumer use tax return for the reporting period during which the transaction subject to the partial exemption occurred. Where the purchaser or retailer fails to claim the partial exemption as set forth above, the purchaser or retailer may file a claim for refund as set forth in subdivision (e).

The purchaser who files an individual use tax return must attach a completed partial exemption certificate to the return. The purchaser who is registered with the Board as a retailer or consumer and files a sales and use tax return or consumer use tax return must, within 45 days of the Board's request, provide the Board access to any and all documents that support the claimed partial exemption.

The partial exemption certificate form set forth in Appendix A may be used to claim the partial exemption.

(e) Refund of Partial Exemption.

(1) For the period commencing on September 1, 2001, and ending on December 31, 2002, a qualified person may claim the partial exemption on qualified purchases from an in-state retailer or an out-of-state retailer obligated to collect the use tax by furnishing the retailer with a partial exemption certificate on or before March 31, 2003. The retailer must refund the tax or tax reimbursement directly to the qualified purchaser of qualified property or, at the purchaser's sole option, the purchaser may be credited with such amount.

(2) A retailer who paid sales tax on a qualified sale or a person who paid use tax on a qualified purchase and who failed to claim the partial exemption as provided by this regulation may file a claim for refund equal to the amount of the partial exemption that he or she could have claimed pursuant to this regulation. The procedure for filing a claim shall be the same as for other claims for refund filed pursuant to Revenue and Taxation Code section 6901. For transactions subject to use tax, a qualified person filing a claim for refund of the partial exemption has the burden of establishing that he or she was entitled to claim the partial exemption with respect to the amount of refund claimed under this part. For transactions subject to sales tax, a person filing a claim for refund of the partial exemption has the burden of establishing that the purchaser of the qualified property otherwise met all the requirements of a qualified person at the time of the purchase subject to the refund claimed under this part.

(f) Improper Use of Partial Exemption.

(1) Property Used in a Manner Not Qualifying for the Partial Exemption. Notwithstanding subdivision (a), tax applies to any sale of, or the storage, use, or other consumption in this state of tangible personal property that is used in a manner not qualifying for the partial exemption under this regulation.

(2) Purchases by Non-Qualified Persons. Notwithstanding subdivision (a), tax applies to any sale of, and the storage, use, or other consumption in this state of tangible personal property if a purchaser is not a qualified person.

(g) Purchaser's Liability for the Payment of Tax.

(1) If a purchaser timely submits a copy of a partial exemption certificate to the retailer or partial exemption certificate for use tax to the Board, and then uses that tangible personal property in a manner not qualifying for the partial exemption, the purchaser shall be liable for payment of the tax, with applicable interest, to the same extent as if the purchaser were a retailer making a retail sale of the property at the time the property was so removed, converted, or used.

(2) A purchaser providing a partial exemption certificate accepted in good faith by the retailer or a partial exemption certificate for use tax to the Board for tangible personal property that does not qualify for the partial exemption is liable for payment of the tax, with applicable interest, to the same extent as if the purchaser were a retailer making a retail sale of the property at the time the property was purchased.

(h) Leases to Qualifying Persons.

(1) Leases—In General. Leases of tangible personal property which are classified as "continuing sales" and "continuing purchases" of tangible personal property, in accordance with Regulation 1660, "Leases of Tangible Personal Property—In General," may qualify for the partial exemption subject to all the limitations and conditions set forth in this regulation. This partial exemption may apply to rentals payable paid by a qualified person on or after September 1, 2001 with respect to a lease of qualified property to the qualified person, which qualified property is used for breeding purposes, notwithstanding the fact that the lease was entered into prior to the effective date of this regulation. For purposes of this subdivision, a non-qualified person may purchase property for resale and subsequently lease the property to a qualified person subject to the partial exemption.

(2) Leases—Acquisition Sale and Leaseback. A qualified person will be regarded as having paid sales tax reimbursement or use tax with respect to that qualified person's purchase of property, within the meaning of those words as they are used in section 6010.65 of the Revenue and Taxation Code, if the qualified person has paid all applicable taxes with respect to the acquisition of the property, notwithstanding the fact that the sale and purchase of the property may have been subject to the partial exemption from tax provided by this regulation.

(3) Subsequent Lease of Property Acquired Subject to Partial Exemption. If a qualified person has acquired property subject to the partial exemption provided by this regulation and has paid all applicable taxes at that acquisition, the property will be regarded as property as to which sales tax reimbursement or use tax has been paid, and the subsequent lease of that property will not be subject to tax measured by rentals payable.

(i) Records. Adequate and complete records must be maintained by the qualified person as evidence that the qualified property was capable of reproduction and purchased by the qualified person solely for breeding purposes.

(j) Operative Date. This regulation is operative as of September 1, 2001.

History—Adopted September 11, 2002, operative September 1, 2001.

Amended June 30, 2004, effective August 18, 2004. Subdivision (a)—in 2nd unnumbered paragraph added phrase "and ending on June 30, 2004," added new third unnumbered paragraph to reflect the increase of the state portion of the sales and use tax to 5.25% on July 1, 2004.

Amended April 15, 2009, effective June 4, 2009. Amended subdivision (a) to reflect the increase in the partial exemption rate to 6.25% from April 1, 2009 until Revenue and Taxation Code sections 6051.7 and 6201.7 cease to be operative.

Amended effective January 9, 2012. Amended subdivision (a) to reflect the decrease in the partial exemption rate to 5.25% on July 1, 2011 caused by the expiration of sections 6051.7 and 6201.7 on June 30, 2011.

Amended March 13, 2013 effective July 11, 2013. Amended subdivision (a) to reflect the increase in the partial exemption rate to 5.50% on January 1, 2013 caused by the addition of section 36 to article XIII of the California Constitution.

Amended September 16, 2015, effective December 16, 2015. Amended subdivision (a) to reflect the one-quarter percent decrease in the partial exemption rate on January 1, 2016 caused by the expiration of Revenue and Taxation Code sections 6051.5 and 6201.5 on December 31, 2015.

Amended January 25, 2017, effective March 9, 2017. Amended subdivision (a) to reflect the one-quarter percent decrease in the partial exemption rate on January 1, 2017 caused by the expiration of the 0.25% sales and use tax imposed by section 36 of article XIII of the California Constitution.

Appendix A